Why should financial institutions tap into the vast SME market?

Small and Medium Enterprises (SMEs) represent the single largest business segment globally. And yet, they’ve also traditionally been the single most underserved segment by financial institutions (FIs) everywhere. This status quo, however, cannot hold – and not merely because growth in other segments has been largely tapped out by traditional financial players.

As new market entrants including neobanks and fintechs disrupt the traditional ways of doing business, they are finding innovative ways to appeal to SMEs while maximizing their ROI.

The time to get on the SME train is now – before the destination becomes overcrowded, as with other financial market segments. Whether you are an established FI or a new market entrant, the question is not if you should play in the SME segment – the only question is how?

We’ve looked at the scope of the opportunity – and it’s big!

Small and Medium Enterprises are typically defined as businesses whose total number of employees falls below a certain threshold. In the US and Canada, that number is typically below 500 employees, with a few industry-based exceptions (e.g. mining, where the threshold is 1500), while the European Union threshold for an SME is below 250 employees.

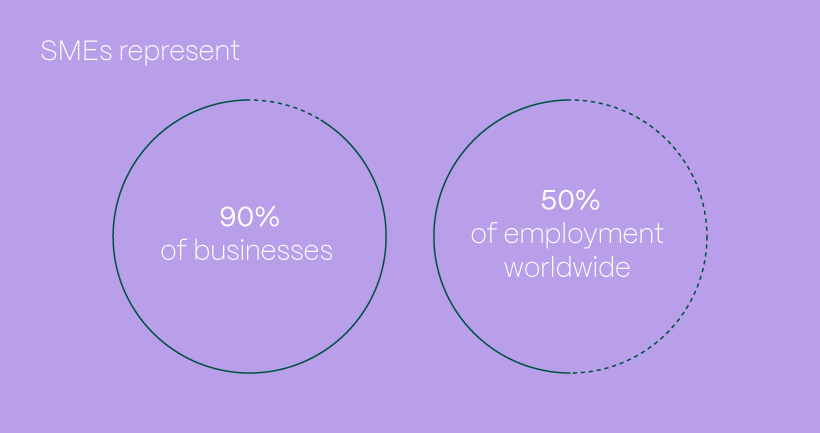

According to World Bank, formal SMEs represent about 90% of businesses and 50% of employment worldwide. The number is significantly higher if non-registered small businesses are taken into consideration. And if you thought that SMEs are only prevalent in developing economies – think again.

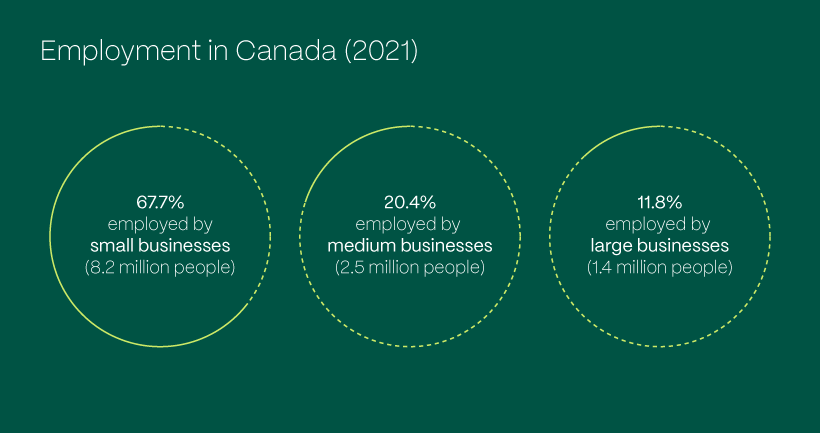

In Canada, small businesses alone employed 8.2 million people in 2021, representing 67.7% of the total private sector labor force. Add to that another 2.5 million, or 20.4%, employed by medium businesses, and then compare it to a mere 1.4 million (11.8%) employed by large businesses, and you’ll get the picture.

And if you thought that SMEs are dominant only in terms of the number of employees, but not revenue generated – a rethinking is warranted yet again. In the European Union, SMEs generate more than half of the European Union’s gross domestic product (GDP).

So, if the opportunity is so sizeable, why are SMEs so underserved?

The challenges in addressing the SME market are not small either – but those who address them will win the prize

Given the number of SMEs alone, they have traditionally been a challenging customer for traditional banks. The cost of serving each SME used to outweigh the return on such investment. SMEs are more demanding than individual consumers, and yet provide a lower return than a large business. Add to that the higher risk profile of SMEs, and you can see why the traditionally conservative large FIs stayed at a distance from such businesses. Structurally, SMEs belonged neither in the consumer divisions of large banks, nor in their corporate counterparts.

This was, of course, all well and good until fintechs and neobanks brought on all the disruption brought. The two single biggest challenges in serving SMEs – as demonstrated above – are the labor-intensive nature of servicing them and their higher risk profile. However, digital technologies have now turned this challenge on its head.

Digital onboarding

The financial institutions – large or small - that have successfully captured the SME market are those who leverage seamless digital customer journeys to attract SME customers.

According to Finalta, top performers in the SME segment onboard 91% of their customers digitally, compared to a mere 17% for other market players. And the benefit is not only in the customer experience aspect – the successful players take only one day to onboard a customer digitally, compared to 8 days for the less successful market players. This means there is a significant reduction in cost-to-serve each SME, resolving one of the most significant challenges associated with the segment.

AI and data analytics for lead generation and customer relationship management

Another aspect of complexity in serving SMEs lies in the fragmented nature of the market segment – making it inherently difficult to understand and address their diverse needs. However, today’s advanced data analytics result in tremendous time savings and greater insights about the segment. Dashboarding, process mapping, and detailed segmentation can be leveraged to optimize lead generation and creation, as well as the entire relationship lifecycle.

Micropayments

The SME opportunity is not limited to banking, either. The payments revolution is a bit late to the table when it comes to SMEs, but the opportunity is ripe. 35% of SMEs feel that the cost of managing their payment cards is significant and noticeable, and a quarter use their personal accounts due to ease of use.

One way to capitalize on the market opportunity in the SME segment is by making reconciliation easier. Again, AI and automation can make this process less cumbersome. Each transaction needs to be categorized for reporting and tax purposes. This is a process executed by finance departments in large organizations. In SMEs, it is a major drain on resources and takes away from their core mission. However, given advances in business process automation, it should now be quite feasible to reduce the effort needed by as much as 90%. Human effort should be required only to review, or QA, rather than categorize transactions.

Integrated Risk Management Technology

Analytics can also be leveraged to better manage risks associated with the SME segment. In the past, banks have stayed away from the segment, largely because their risk management processes were not sophisticated enough to manage such a fragmented segment.

These days, integrated risk management technology allows for dynamic management of risk in near real-time. Sophisticated third-party data, coupled with data gathered from customer relationship management processes that are part of the customer digital journey, can provide proactive insights on areas to pursue – and avoid.

Build your SME offering with the right partner

The SME market and the digital revolution are about to converge and open up this vast opportunity to those who get the solution right. If you need help in building your SME offering, you should look for a partner with technical expertise in advanced digital technologies as well as deep domain knowledge in financial services and fintech.