Tokenised payments are no longer optional: Why banks and merchants must act before 2030

Digital payments are evolving fast, driven by consumer demand for speed, security, and convenience.

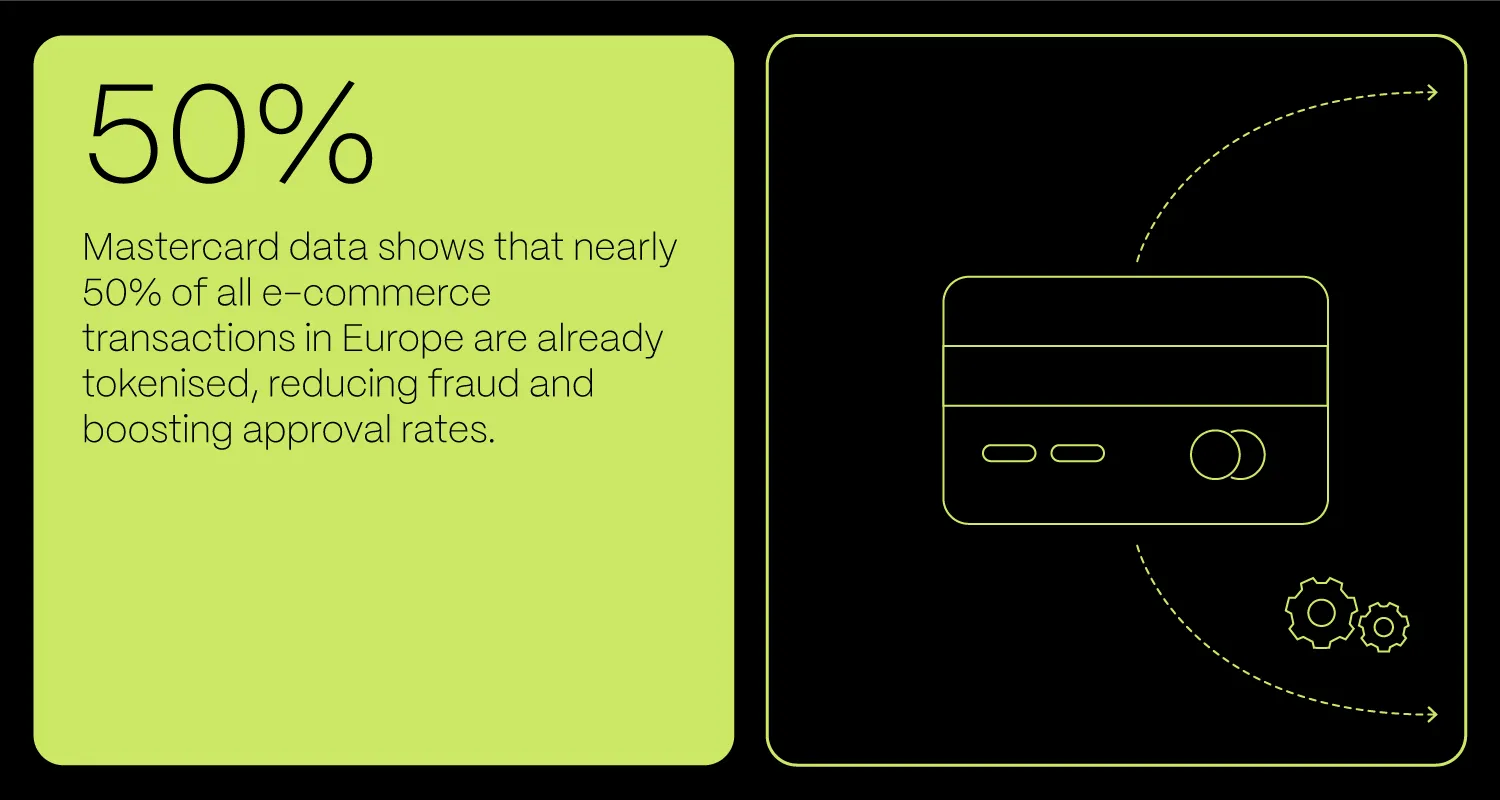

Statistics prove the same. Mastercard data shows that nearly 50% of all e-commerce transactions in Europe are already tokenised, reducing fraud and boosting approval rates.

More on tokenised payments, their importance, and implementation below.

What are tokenised payments?

Tokenised payments replace sensitive card details, such as the 16–19 digit number printed on your card, with a unique, non-sensitive token used to process the payment. Unlike the real card number, this token is tied to a specific device, merchant, or even a single transaction. If intercepted, it is useless to fraudsters.

Chances are you have already used tokenised payments without realising it. Paying with Apple Pay or Google Pay in a shop, completing a one-click online checkout, or letting your favourite streaming service bill your saved card each month – believe it or not, all of these rely on tokenisation. The same applies to ride-hailing apps like Uber, where your card details are stored securely yet never actually transmitted during the transaction.

The best thing is that the result is the same no matter the channel.

Why tokenisation matters now

Visa and Mastercard have both set a goal to make all payments tokenised by 2030. For banks and merchants, this is becoming a requirement. So, let’s take a look at some of the core benefits of tokenisation:

- security: Your sensitive details never leave the safety of your bank or payment network, while your purchase goes through just as quickly as if you had typed them in yourself, only without any risk. Unsurprisingly, that is how the risk of fraud is minimised.

- user experience: Tokenisation unlocks the potential of smoother payment journeys, such as one-click checkouts, NFC mobile payments, and automatic renewals for subscriptions. Customers no longer need to re-enter their card details for every purchase, which reduces friction and increases the likelihood of completing the transaction.

- compliance: By removing the need to store or transmit actual card numbers, tokenisation makes it easier for businesses to meet regulatory requirements such as PCI-DSS, PSD2, and Strong Customer Authentication (SCA). In that way, it reduces the compliance burden while maintaining high security standards.

- approval rates: Because tokenised transactions are considered lower risk, card issuers are more likely to approve them. This not only improves the customer experience but also increases revenue for merchants by reducing failed payments.

- future readiness: Implementing tokenisation now creates the technical foundation for future payment innovations. It positions businesses to easily adopt digital wallets, embedded finance solutions, and tokenised currencies such as central bank digital currencies (CBDCs) and stablecoins.

SEE banks and the state of tokenisation

Without integrating Visa Token Service or Mastercard Digital Enablement Service, banks won’t be able to support token provisioning for Apple Pay, Google Pay, and similar services.

What does that mean for customers? Well, they won’t definitely wait around when another bank can give them that convenience and security right away.

So, the clock is ticking. And, both financial institutions and ecommerce merchants without “token-ready” systems could find themselves on the sidelines.

Regional momentum and modernisation efforts

Banks across Southern and Eastern Europe are moving fast to modernise their systems, with big investments in cloud technology, real-time payment processing, and AI. Instant payments and slick digital banking apps are now fairly common, but card tokenisation is still catching up.

The Pan-Europe impact

Mastercard says nearly half of all e-commerce transactions in Europe are already tokenised, and its Secure-on-File service is available in 45 countries, SEE markets included. Even if local banks aren’t shouting about their progress, many are quietly rolling out tokenisation behind the scenes, often in partnership with payment networks or tech providers.

Wholesale and CBDC initiatives

It’s not just about paying for your morning coffee with a phone tap. Some banks are experimenting with tokenised deposits, exploring blockchain-based settlements, and building wholesale payment rails for bank-to-bank transfers. These projects tie into broader European efforts to create safer, faster, and more connected digital payment systems.

The role of a tech partner in tokenised payments

But behind every smooth mobile payment or one-click checkout lies a complex web of integrations, APIs, compliance layers, and user flows that must be carefully built and orchestrated.

This is where software development companies like Vega IT play a critical role.

So, what does that mean for each stakeholder?

For e-commerce businesses

In online shopping, every extra second at checkout increases the risk of losing a customer. Nearly 70% of shopping carts are abandoned before purchase. That is why for e-commerce businesses, enabling a fast and secure checkout is not just a nice-to-have anymore. It is essential.

This is often achieved through payment gateways like Stripe, Adyen, or Checkout.com, which handle tokenisation and other security processes.

Each comes with its own APIs, flows, and best practices, and getting them right is critical for both user experience and compliance. That is where a skilled enterprise integrations partner can step in to design the right architecture, choose the most suitable integrations, and implement them so everything runs smoothly from front-end to back-end.

For banks

For banks, this complexity is even greater. Issuers must integrate with major card schemes, manage the full token lifecycle, and connect with mobile wallets. Many mid-tier banks still rely on legacy cores and third-party processors, making tokenisation a challenge. In this case, they need to build the integration layers, map data, implement encryption, and orchestrate connections between card networks, fraud systems, and mobile apps.

The hardest part, however, isn’t always the code. It’s often the compliance. Meeting PCI-DSS standards, aligning with EMVCo specifications, passing Visa/Mastercard certifications, and ensuring PSD2/SCA compatibility requires both domain expertise and precise execution.

Forward-looking projects go beyond basic enablement. Token vaults, merchant dashboards, analytics for approval rates, and support for emerging payment methods all form part of a future-proof tokenisation strategy.

Acting now matters

Tokenised payments are becoming a part of our everyday lives. And, the businesses that act early will see higher approval rates, lower fraud, and smoother checkouts and will be ready for the payment ecosystems of the next decade.

Want to learn how the right implementation partner can make that transition faster and safer for you? Contact us.