Open banking and A2A payments in the US: Evaluating the potential hurdles and upsides

Out of all the use cases for A2A payments, the B2B channel may be key to unlocking the market potential in the US.

In a major move intended to jumpstart competition and accelerate the shift to open banking, the US Consumer Financial Protection Bureau (CFPB) has proposed a set of rules that will require financial institutions to share their customers’ data with other financial institutions upon customers’ request. This shift to open banking would ultimately require the US financial institutions (FIs) to consider and stay ahead of potential disruptions in the market.

Given that Europe initiated the move to open banking in 2015, the EU represents an excellent case study as the US FIs consider the applicable threats and opportunities. My software development organization, Vega IT, has extensive experience supporting the implementation of open banking in Europe. Furthermore, my multi-decade North American and European payments industry experience provides me with a unique perspective on the upsides of open banking. In this article, I’ll apply this lens to potential hurdles and upsides of one prominent feature of the European open banking system – account-to-account (A2A) payments.

Firstly, I’ll summarize the potential benefits of A2A payments, then we’ll consider the current state of the European and US markets in this regard, and finally, evaluate some use cases that could be compelling in the unique context of the American market.

A2A payments have potential benefits for businesses and consumers alike

A2A payments are payments made directly from one bank account to another. What distinguishes A2A payments from the most commonly seen transactions in the US is that they cut out the intermediary such as a credit or debit card.

In the EU, open banking regulations obligate financial institutions to make account information and payment initiation accessible via API to other licensed third-party providers if the account holder wishes. This allows these other licensed providers to create A2A payment platforms and compete for market share by offering users lower costs, unique value-added features, and superior service quality.

In Europe, this mode of payment has found fertile ground in many use cases. For example, a consumer may want to split a bill with friends without using cash, pay their plumber, or even a major merchant at the Point of Sale – whether online or brick-and-mortar. Businesses may pay each other directly for services rendered. In all of these cases, if well executed, there are certain potential benefits to both consumers and businesses unique to A2A payments.

For businesses, these benefits include higher conversion rates given the ease of use, reduced transaction costs given that no card issuer fees are involved, faster payment times with no intermediaries, and access to more customers – not only those with a valid credit card. Consumers like A2A because they can complete online purchases with one click rather than type in card numbers over and over (and over), and they do so safely using multifactor authentication by their bank, such as FaceID.

While these benefits have made A2A payments highly successful in some areas of the EU, some may actually represent a drawback in the US market. This is why it’s important to take a look at some similarities and differences between the two markets as they relate to A2A payments before coming to conclusions about their US market potential.

Europe and the US: A tale of two markets

A slowing global economy has had an impact on the banking markets in both Europe and the US, and we can certainly expect this to continue in much of 2024. According to Deloitte, this will further exacerbate the FI disruption from generative AI, industry convergence, embedded finance, open data, digitization of money and identity, and decarbonization. While the FI business model tends to be relatively stable, modest organic growth coupled with the depressionary impact of the factors named above will drive the pursuit of creative ideas for new revenue streams.

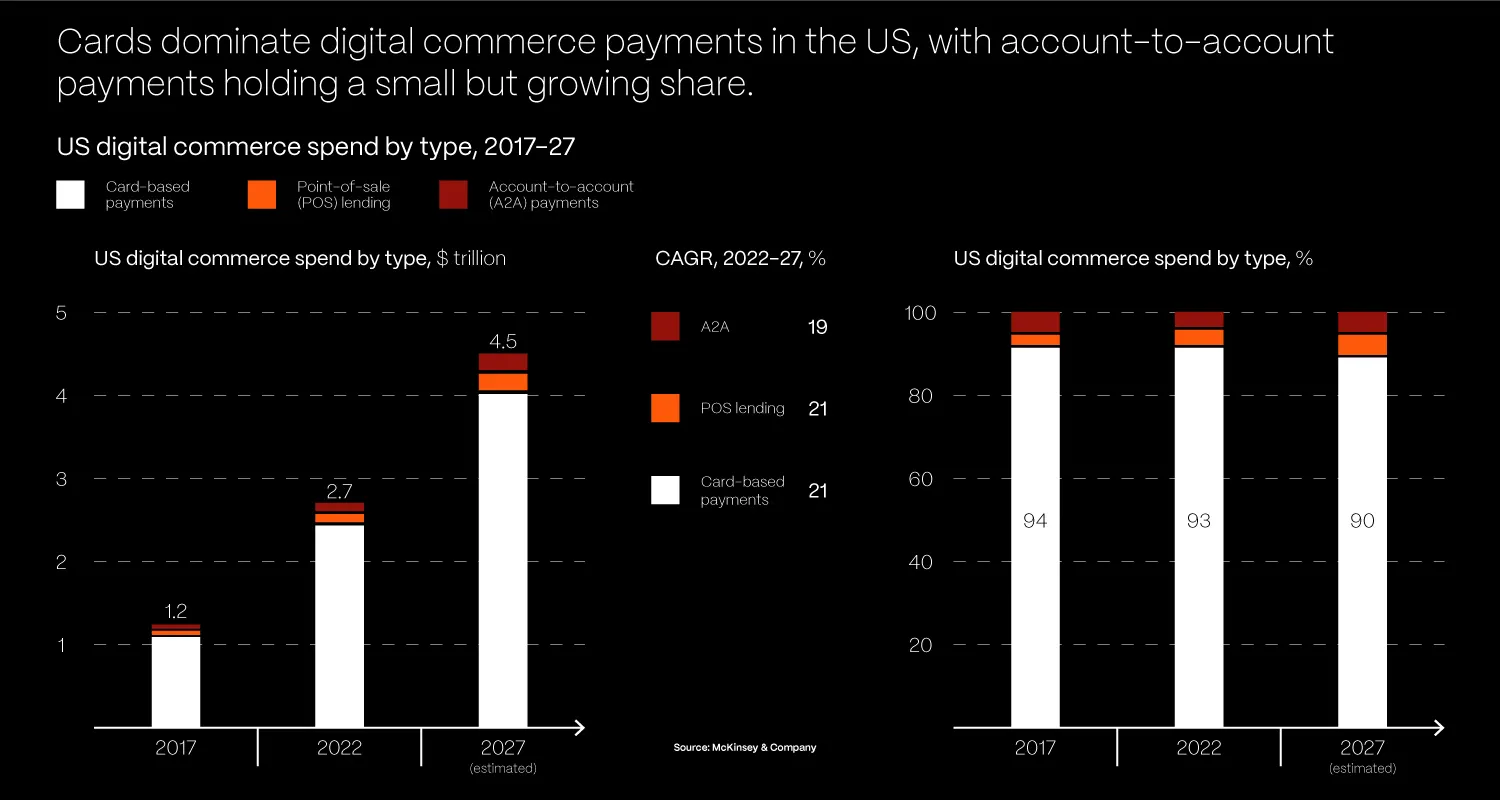

Globally, A2A payments accounted for 9% of all e-commerce payments and represented $525B in 2022, according to Neonomics. Europe is clearly an early adopter, with 18% of A2A transaction share. The sharp rise in A2A payment adoption outside the US is driven by rising card payment processing costs, along with the benefits of A2A payments to businesses and consumers that I’ve outlined in the previous section. The success of A2A payments in certain parts of Europe makes it a great primer for US FIs pondering their next move in this space.

However, there are substantial differences to be considered between the markets, as well. Culturally, European consumers have been hesitant adopters of credit card payments, while this mode of payment is ubiquitous in the US. As McKinsey points out, “Americans love their credit cards and the rewards that come with them, so dislodging the popularity of cards is perhaps the biggest challenge to US adoption of A2A.”

The current share of A2A payments in the US paints a bleak picture compared to Europe – so what are the potential upsides?

Evaluating areas of the US market that could provide fertile ground for A2A payments

The McKinsey article I cited above is very direct in stating that the A2A value proposition is “more merchant-friendly than consumer-friendly” as it lacks “charge-back protections; provides no credit, float, or rewards; and can add friction by requiring consumers to enter their banking credentials for each transaction.” And so, it is important for the US FIs to be realistic and methodically evaluate the potential of each A2A payments use case when determining their strategy as it relates to open banking. I’ll evaluate some of the main use cases below, applying my experience in both the US and European contexts.

C2C (person-to-person) payments

There are already some C2C payment services in the US, the most familiar of these being Zelle.

Zelle has captured the person-to-person A2A use case with an instant service directly accessing the consumer’s bank account. What is important to note is that Zelle is initiated from a consumer’s bank, and so remains closed to FinTechs. FinTechs have had to work around the absence of open banking regulations by relying on a stored value account to complete transactions, this being an additional hassle to consumers, which allowed Zelle to outgrow the market.

With mandated APIs for payment initiation and account data access, fintechs may well be able to play on par with Zelle when using the TCH’s RTP and FedNow real-time payment networks. However, to meaningfully gain market share on Zelle, FinTechs pursuing this use case scenario for A2A payments will need to offer additional unique benefits over-and-above the capability currently offered by Zelle. As of yet, it is not at all clear what these unique benefits would be.

B2C disbursements

With the rise of the gig economy and online marketplaces, business-to-consumer payouts are gaining a more prominent place in the broader payments market. This has not gone unnoticed by card networks, who are already playing in this field through services such as Mastercard Send and Visa Direct.

With Zelle and TCH’s real-time payments (RTP) network also pursuing this use case, there is clearly an opportunity for more true A2A solutions as the banking market opens up to FinTechs. If FinTechs are able to provide lower-cost service than card networks in real time, they may be able to capture a piece of the B2C disbursement pie – this being a rather significant “if.”

C2B payments

In this use case, the EU and UK provide some examples of successful A2A payment scenarios that may be of interest to US businesses. With open banking, third parties can become payment-initiation-service-providers (PISPs) and move money from a consumer’s account to a merchant’s account by way of a real-time rail.

The benefit to businesses in this scenario is clear – lower cost and instant payment. However, it is difficult to see the benefit to the consumer that would render this use case a success in the US. Just think of MCX, a payment network established by a consortium of some of the US’s most prominent retailers with over $1 trillion in sales, including 7-Eleven and Walmart. Despite the massive market share held by these retailers and investment to match MCX was not a success, as cards offer significant benefits to the consumer and are firmly entrenched in American consumer culture. This case study raises significant doubts about the potential success of A2A C2B payments in the US.

B2B payments

What I firmly believe to be the use case with the strongest potential in the US is the B2B market, which is currently served by a number of legacy payment methods, including commercial cards, ACH, and paper checks.

With credit cards, the payer benefits from immediate payment but the payee bears the cost. On the other hand, with ACH, there is certainly a lower cost, but also limited information content and slower settlement. Paper checks are ubiquitous but extremely slow for today’s fast-paced world as well as prone to fraud.

An A2A solution could be a game changer for businesses, offering the benefits of each of the three currently used payment methods while eliminating their drawbacks. Leveraging a real-time payment network along with an ISO2022 standard for remittance data (which is crucial), this solution truly meets the needs of today’s business by enabling:

- Automated reconciliation of incoming payments with outstanding invoices, which eliminates most of the manual administration costs associated with B2B payments;

- Easier payment tracking, issue resolution, and system reconciliation for customers and financial institutions, which, in addition to eliminating the administrative burden, reduces financial losses; and

- Consistency in providing remittance information between e-procurement platforms, unlocking the tech platform ROI for all parties.

Currently, many businesses employ accounts receivable and accounts payable administrators to administer, reconcile, and troubleshoot payments. If software systems are used, remittance data such as the payee’s name, address, and invoice number are lumped together, requiring manual or additional technical intervention. Structured remittance data based on the ISO2022 standard using real-time payment rails solves all of the above issues.

So, if A2A payments leveraging open banking are to take hold in the US, my estimation is that it will be by way of B2B payments, given the massive benefits to businesses. As this happens, FIs and fintechs alike may get creative to develop new and unique benefits for consumers, thereby expanding the potential for market success. However, given the differences between the European and US markets, success is not a given.

FIs and fintechs should not ignore the A2A payments potential in the US. At the same time, they must carefully consider the potential use cases in the US context and choose an entry point with the least amount of potential friction while applying as much creativity as they can to their success. We offer our clients unparalleled domain expertise covering systems, solutions, and business models across financial services value chains. Your success. Our passion. Get in touch.

Download free whitepaper: Capitalizing on the embedded finance revolution

While it simplifies the lives of consumers everywhere, the embedded finance proposition is not a simple one to grasp from an investment perspective. Is embedded finance a fad or a revolution? And how should you approach it - whether you’re an established FI or a fintech looking to make its mark?

Download whitepaper