B2B fintechs' fast track to profitability in 2023: Exceptional solutions for single participants in complex value chains

Leaders of B2B fintech companies, along with the large financial institutions they target as customers and investors, are facing unique economic headwinds - a confluence of high inflation and reduced economic growth. These headwinds are further exacerbated by ongoing competition for talent in a labour market where low unemployment figures are still the norm.

The current crisis will surely create major challenges for many tech companies – B2B fintechs included - as their access to funding is more difficult and expensive, and their target customers reduce spending. However, this also presents a unique opportunity to produce a truly differentiated offering tailored for the current times, which will be a gamechanger for both the B2B fintechs and their customers and investors alike. Fintechs can succeed by pivoting their focus away from targeting long-term, exponential growth and towards more immediate revenue and profit generation.

Understanding the current crisis is the first step in not letting it go to waste: where is the opportunity?

Decreased vendor spend and investment volume will have a profound effect on the fintech ecosystem.

From an investor's point of view, the promise of long-term exponential growth doesn't look as appealing as it once did. Due to inflation, valuations of growth companies are down as their future revenues and profits have lower net present value. Investors are now looking for companies that generate profit in the near term, rather than those with exponential growth potential.

Similarly, the financial institutions B2B fintechs target as potential customers have a reduced risk appetite. Reducing spend is a priority when weathering a crisis. Stagflation - let’s call the current crisis by its true name - is the ultimate catch-22 because it couples recessionary pressures with high inflation, and the traditional solutions for one side of the equation necessarily exasperate the other. There is no proven magic pill; the risks are high. All of this is “Economics 101”, but also the key to understanding how large financial corporations will act in this time of heightened risk - the answer being “very conservatively”.

Another catch-22: in addition to lowering their overall vendor spend due to the confluence of economic risks I described, there is also significant risk for the established financial players in letting a “good crisis go to waste”, as famously phrased by Winston Churchill. A competitor may use the shifting landscape as an opportunity to redefine the game, and nobody wants to be left behind - or, even worse, outside.

So, large financial institutions and fintechs alike will seek a delicate balance between the need to promptly reduce investment/vendor spend risk, and their need to invest in products and solutions that will enable them to generate new revenue streams, win market share and/or transform through innovation as the economy picks up.

Shorten your sales cycle while accelerating ROI: keep it simple!

What does this shift in focus away from prioritizing long-term, exponential growth and towards quicker wins mean for B2B fintechs?

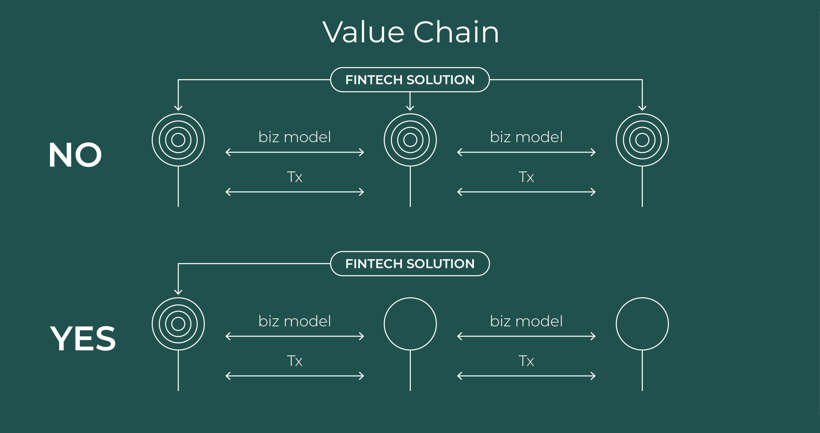

Sales cycles with large financial institutions are notoriously lengthy, even in the best of times. This problem is further exacerbated by fintechs’ appetite for transformative impact that requires disruption of complex, well established value chains. Most fintechs fail due to the difficulty of selling and implementing solutions that require multiple large players in the value chain to agree to do the same thing at the same time.

Established players have made a significant investment in their current state - and they don’t feel the need to fix it if it’s not fundamentally broken. Any significant change to the status quo also presents a risk for each player in the value chain - they may lose competitive advantage and/or a competitor may adapt to change better, resulting in loss of market share.

One approach to transcending the complexity of selling into established value chains is to skip them all together. The best way to achieve success for B2B fintechs is to solve an existing, persistent problem extremely well for a single large, influential player rather than get bogged down in the politics of complex value chains with multiple players while selling vague promises of future exponential growth.

This ensures their solution will be implemented without dependency on other players in the value chain. Whether your solution provides better efficiency or lower cost, better user experience, or new features that open up additional revenue streams, it should do it extremely well, and as quickly as possible.

The talent war is over, and talent won: turn your employees and service providers into your competitive advantage!

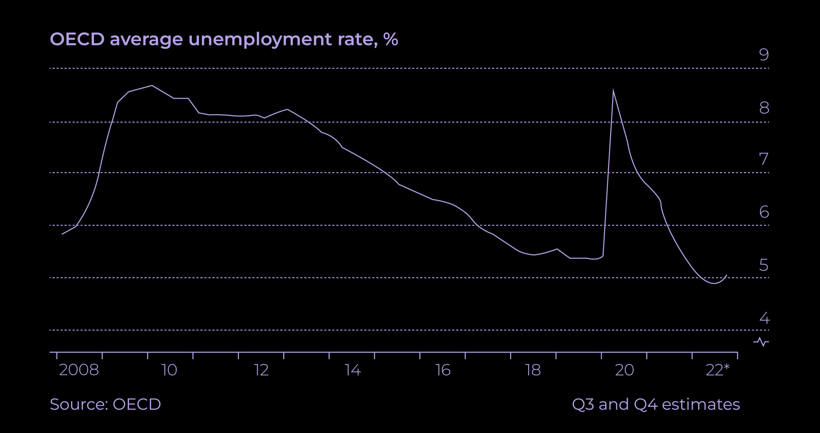

There is another feature of the current crisis that presents a unique opportunity for fintechs - namely, while economic activity is significantly slowing, unemployment continues to be at a record low, and creative talent with the right domain expertise is difficult to find.

As a recent article in The Economist points out, The world in brief, Jan 3rd, 2023. ("Labour markets are the bright spot in the world economy"), after the 2008 financial crash, the rich world’s unemployment rate rose from 5.8% to 9%. Yet, the most recent numbers released in the US and elsewhere indicate the opposite problem in the form of shortage of talent. While employment growth has admittedly slowed down somewhat, it would take an awful lot to reach the employment lows of early 2010s from the current unemployment level of 4.9% across the rich world.

So - the talent war was indeed won by talent, as PwC's US chair Tim Ryan recently pointed out, grabbing headlines with the new catchphrase. By extension, fintechs who either employ, or establish partnerships with those who offer talent capable of creating value in a time of crisis rather than merely "getting the job done" - are more likely to become winners as well.

Fintech companies often have limited resources and may find it easier and more cost effective to partner with the right talent provider. Organizations such as my own, Vega IT, work with both fintech startups and financial institutions. Therefore, they possess a unique combination of understanding the strengths and weaknesses in the existing systems and business models, and the ability to target these strengths and weaknesses by co-creating value through emerging technologies.

Whether by hiring talent, or partnering with the right software company with domain expertise, the truly successful B2B fintechs in the present crisis will develop innovative and targeted solutions with strong value propositions for a single influential large player - shortening their sales cycle while delivering prompt ROI for their customer.

What are you doing to ensure your B2B fintech company doesn’t let the current crisis go to waste? I would love to continue the discussion on this platform, or at nebo@vegaitglobal.com.